Major financial institutions are facing a pivotal shift as cryptocurrencies transform global finance. The integration of digital assets is redefining payment systems, capital markets, and risk management, affecting every aspect of portfolio strategy. For institutional investors and financial analysts, understanding crypto’s structural role—from cross-border efficiency to regulatory evolution—guides smarter investment decisions and ensures readiness for the next phase of financial innovation.

Key Takeaways

| Point | Details |

|---|---|

| Institutional Integration | Adopting cryptocurrencies is crucial for institutions to stay competitive, with integration into existing financial systems necessary for long-term success. |

| Regulatory Clarity | Clear regulations pertaining to custody and market conduct are vital for institutional adoption of crypto assets, enabling capital deployment into digital assets. |

| Diverse Crypto Categories | Institutions should evaluate different crypto categories, such as Bitcoin, Ethereum, and Stablecoins, to determine which assets align with their investment strategies. |

| Risk Management Frameworks | Robust risk management protocols must be established to address the unique challenges posed by the integration of crypto assets with traditional financial systems. |

Defining Crypto’s Role in Global Finance

Cryptocurrencies have moved beyond speculative assets into a structural component of modern finance. Institutions now recognize them as digital assets with measurable economic impact on payment systems, financial inclusion, and capital markets.

The fundamental shift involves understanding what cryptocurrencies actually do. Unlike traditional currencies, they operate on decentralized networks without intermediaries, enabling direct peer-to-peer transactions across borders. This creates new possibilities for institutions managing global operations.

The Economic Impact

Crypto’s role encompasses multiple dimensions that directly affect institutional strategy:

- Cross-border efficiency: Reduced settlement times from days to minutes, cutting operational costs for international transactions

- Financial inclusion: Access to banking services for unbanked populations without traditional infrastructure

- Market transparency: Immutable ledgers create permanent transaction records, reducing fraud risk

- Alternative assets: New investment classes that don’t correlate directly with equity or bond markets

Research on macrofinancial implications of crypto assets shows both substantial benefits and systemic risks that require institutional consideration.

Integration With Traditional Finance

The boundary between crypto and traditional finance continues blurring. Institutions face a critical decision: integrate or risk obsolescence. Major banks now offer custody services, trading desks operate 24/7, and blockchain technology upgrades existing infrastructure.

Stablecoins represent a practical bridge between worlds. They combine crypto’s efficiency with dollar stability, enabling institutions to move capital quickly without volatility concerns. This hybrid approach appeals to risk-averse institutional investors managing large portfolios.

Centralized digital currencies add another layer. When central banks issue CBDCs, they validate blockchain technology’s utility while maintaining monetary control—a framework institutions must prepare for immediately.

Strategic Considerations

Institutional adoption hinges on four factors:

- Regulatory clarity on licensing, custody standards, and reporting requirements

- Operational infrastructure supporting trading, settlement, and compliance

- Risk management protocols addressing volatility and counterparty exposure

- Talent acquisition to build teams understanding both finance and blockchain

Institutions that delay crypto integration face competitive disadvantage as market infrastructure matures around these technologies.

The transformation isn’t about replacing traditional finance—it’s about creating parallel systems that interact. Your institution’s role depends on client demand, risk tolerance, and competitive positioning within your market segment.

Pro tip: Start by mapping which institutional services gain efficiency from blockchain settlement (custody, corporate actions, margin lending) before building comprehensive crypto strategies that address your entire client base.

Major Crypto Types and Market Use Cases

Cryptocurrencies aren’t monolithic. Each type serves different institutional purposes, from settling payments to enabling complex financial contracts. Understanding these distinctions directly impacts which assets your institution should evaluate first.

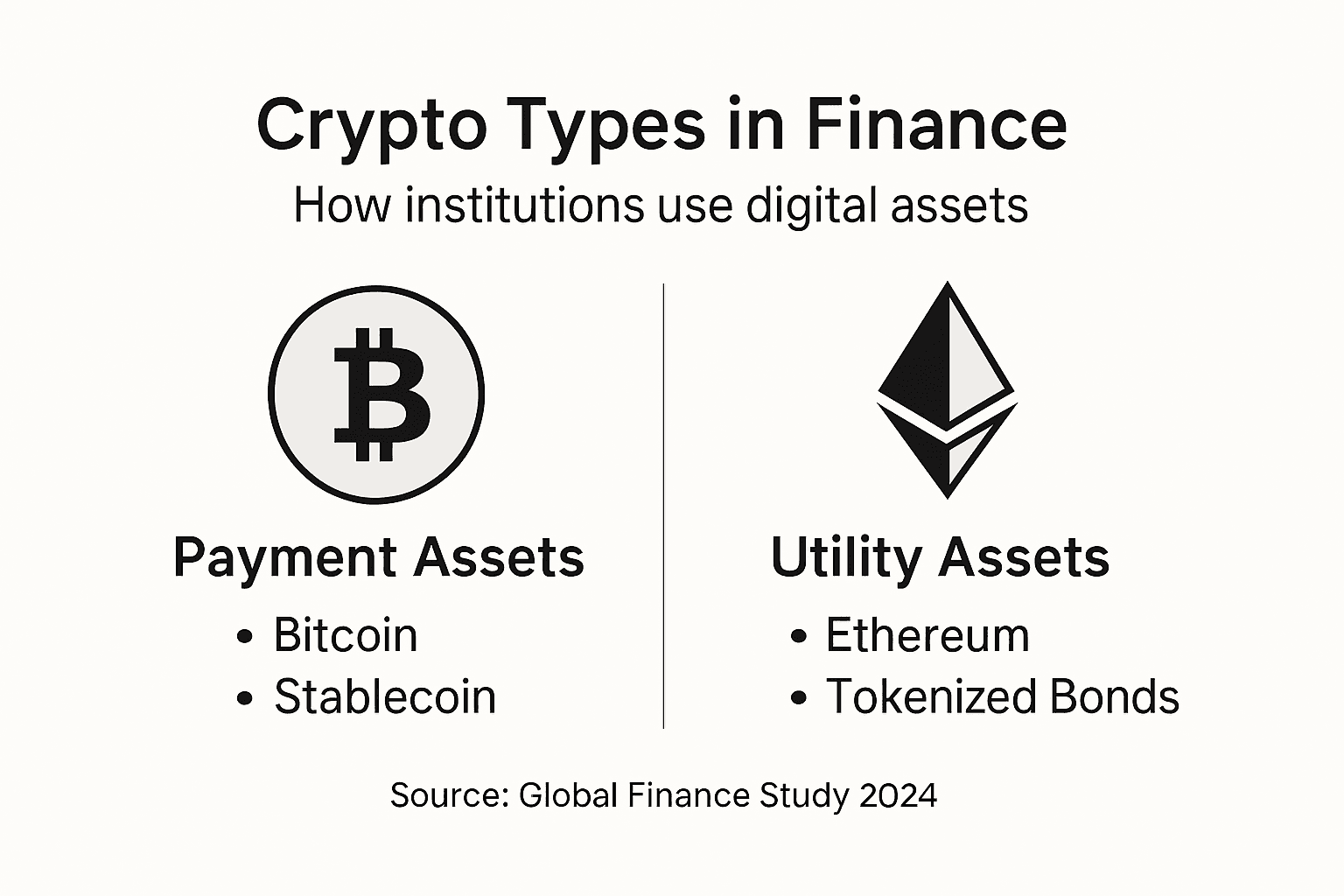

The crypto ecosystem divides into clear categories based on function and market maturity. Bitcoin dominates as store of value. Ethereum powers programmable applications. Stablecoins bridge crypto and traditional finance. Each addresses specific institutional needs.

Primary Crypto Categories

- Layer 1 blockchains (Bitcoin, Ethereum): Foundation networks enabling transactions and smart contracts

- Stablecoins: Dollar-pegged tokens reducing volatility for institutional treasuries

- Decentralized Finance (DeFi) tokens: Assets powering lending, trading, and liquidity protocols

- Central Bank Digital Currencies (CBDCs): Government-issued digital currencies gaining traction globally

Institutions evaluate cryptocurrency types and attributes including volatility, liquidity, and settlement speed when building exposure.

The main crypto asset types serve distinct institutional purposes:

| Asset Type | Primary Role | Maturity Level |

|---|---|---|

| Bitcoin | Store of value, settlement | Most established |

| Ethereum | Programmable apps, contracts | Rapidly growing |

| Stablecoins | Payment, bridge to fiat | Fast adoption |

| DeFi Tokens | Lending, liquidity, funds | Emerging |

| CBDCs | Government-backed settlement | Trial/early rollout |

Bitcoin as Institutional Reserve

Bitcoin’s scarcity and 15-year track record appeal to treasurers managing billion-dollar portfolios. Major corporations and pension funds now hold Bitcoin as portfolio diversification. Its uncorrelated returns reduce overall risk when combined with stocks and bonds.

Settlement happens on-chain in roughly 10 minutes, eliminating counterparty risk during transfer. This attracts institutions managing large transfers between subsidiaries across jurisdictions.

Ethereum and Smart Contract Utility

Ethereum enables programmable money—contracts that execute automatically when conditions are met. Insurance firms use smart contracts for claims processing. Real estate companies tokenize property ownership. Supply chain operators track goods with immutable records.

This flexibility makes Ethereum essential for institutions exploring blockchain beyond simple payments. The network processes thousands of transactions daily from institutional users.

Stablecoins as Bridge Assets

Stablecoins combine blockchain efficiency with price predictability. Major institutions use them for rapid capital movement without exposure to volatility. Redemption features guarantee 1:1 conversion to dollars, eliminating liquidity risk.

Stablecoins solve the volatility problem that prevented institutional adoption of earlier cryptocurrencies.

They function as on-ramp assets for institutions entering crypto markets. Your treasury can move dollars into stablecoins, execute transactions within minutes across borders, then convert back to fiat currency.

DeFi and Tokenized Assets

Decentralized finance protocols now manage billions in institutional capital. Treasurers earn yield on stablecoin reserves through lending pools. Asset managers create tokenized funds accessible 24/7 without intermediaries.

Tokenization extends beyond currencies to real-world assets—real estate, commodities, bonds. Crypto assets tokenize securities that previously required traditional settlement infrastructure.

Pro tip: Start with stablecoins and Bitcoin before exploring DeFi opportunities, as these assets have established custody infrastructure and regulatory clarity that institutional risk committees require.

Institutional Adoption and Regulatory Evolution

Regulatory clarity determines institutional adoption speed. Without clear rules, risk committees block crypto initiatives. With frameworks in place, institutions move capital aggressively into digital assets. The regulatory landscape shifted dramatically between 2020 and 2024.

Major jurisdictions now recognize crypto’s role in financial systems. The United States, European Union, and United Kingdom each developed distinct approaches balancing innovation with consumer protection. Institutions watch regulatory developments as closely as market prices.

The Regulatory Turning Point

Early crypto regulation focused on consumer warnings and restrictions. Today’s frameworks enable institutional participation while maintaining safeguards. Evolving crypto regulations across jurisdictions now address custody standards, market integrity, and systemic risk.

This shift matters immediately to your institution. Clear rules remove legal uncertainty that previously deterred conservative investors. Pension funds, insurance companies, and asset managers can now justify crypto exposure to boards and regulators.

Key Regulatory Developments

Regulatory frameworks now address:

- Custody standards: Institutional-grade asset protection requirements

- Market conduct: Anti-manipulation and transparency rules for trading platforms

- Anti-money laundering: Know-your-customer and transaction monitoring obligations

- Consumer protection: Stablecoin backing requirements and disclosure mandates

Institutions require regulatory certainty before deploying significant capital. Ambiguity kills deals. Clarity unlocks billions in institutional interest.

Global Divergence in Approach

The European Union implemented MiCA (Markets in Crypto-Assets Regulation) creating unified standards across member states. This removed jurisdictional arbitrage that created compliance nightmares for multinational institutions.

The United States pursued sector-specific regulation through existing frameworks. The Securities and Exchange Commission oversees crypto securities. The Commodity Futures Trading Commission regulates crypto derivatives. This creates complexity but allows innovation within defined guardrails.

The United Kingdom developed a phased regulatory approach. Stablecoins received priority attention. Spot Bitcoin and Ethereum trading now operate under established rules. This pragmatic sequencing enabled rapid institutional adoption.

Here is a summary of how leading jurisdictions approach crypto regulation:

| Region | Core Approach | Institutional Focus | Regulatory Body |

|---|---|---|---|

| United States | Sector-specific rules | Crypto securities, derivatives | SEC, CFTC |

| European Union | Unified regulation (MiCA) | Custody, market standards | ESMA, ECB |

| United Kingdom | Phased, asset-priority | Stablecoins, spot trading | FCA, Bank of England |

Institutional Risk Committees and Compliance

Institutional adoption accelerated when regulatory frameworks provided compliance clarity around custodial requirements and operational standards. Risk committees can now justify crypto allocations using precedent from regulated financial products.

Custody became the pivotal issue. Institutions won’t hold crypto without institutional-grade security. Qualified custodians operating under regulatory oversight removed this barrier. Major financial institutions now offer crypto custody services.

Regulatory clarity on custody and market conduct transformed crypto from speculative asset to institutional holding.

Compliance teams shifted focus from whether to participate to how to participate safely. This represents fundamental acceptance by traditional finance.

Looking Ahead

Central bank digital currencies validate blockchain technology’s utility. When central banks issue CBDCs, they establish regulatory precedent that institutional adoption follows naturally. This creates institutional opportunity windows lasting months, not years.

Pro tip: Build your compliance framework now based on your primary jurisdiction’s regulations rather than waiting for perfect global harmonization, as institutional-grade crypto infrastructure in your region creates first-mover advantage opportunities.

Investment Opportunities, Risks, and Tax Implications

Crypto investments deliver genuine portfolio benefits alongside material risks. Understanding both sides determines whether your institution allocates capital or passes. The opportunity is real. The downside risks are equally substantial.

Bitcoin and Ethereum show low correlation with stocks and bonds. This diversification benefit attracts institutional investors managing billions across asset classes. However, volatility remains significantly higher than traditional investments. One bad regulatory announcement can trigger 20% daily losses.

Portfolio Diversification Benefits

Crypto allocation provides measurable diversification advantages:

- Low correlation with equities: Price movements differ from stock markets, reducing overall portfolio volatility

- Inflation hedge characteristics: Some institutional investors use Bitcoin as insurance against currency debasement

- Alternative yield opportunities: DeFi protocols generate returns unavailable in traditional fixed income

- Emerging market exposure: Crypto enables access to growth in developing economies without currency risk

Institutions typically allocate 1-5% of portfolios to crypto, treating it as alternative asset class alongside hedge funds and private equity.

Volatility and Liquidity Challenges

Crypto volatility exceeds most financial assets. Bitcoin fluctuates 30-40% annually while stocks average 15-20%. During market stress, crypto asset volatility can spike above 80% annualized, creating margin call risks for leveraged positions.

Liquidity varies dramatically by asset and market. Major exchanges offer tight bid-ask spreads for Bitcoin and Ethereum. Smaller altcoins suffer wide spreads, making large trades expensive. Your institution needs institutional-grade liquidity infrastructure, not retail exchange access.

Regulatory and Compliance Risks

Regulatory changes instantly impact valuations. When the SEC signals enforcement action against staking platforms, affected assets decline 15-25% within days. Your compliance framework must address regulatory scenarios across multiple jurisdictions.

Three critical risks require monitoring:

- Jurisdiction changes: New regulations can restrict institutional participation overnight

- Tax treatment shifts: Capital gains classification changes affect return calculations

- Exchange restrictions: Trading bans in major economies reduce liquidity immediately

Tax Implications Across Jurisdictions

Tax treatment creates institutional headaches. Crypto tax frameworks evolve rapidly across countries, requiring continuous compliance updates. The United States treats crypto as property, not currency, generating capital gains tax on every transaction.

The European Union applies VAT to crypto exchanges in some jurisdictions but not others. Singapore taxes crypto gains as income. Switzerland treats crypto holdings as taxable assets requiring annual valuations.

Your institution needs tax advisors in each jurisdiction where it holds crypto. A single misclassification triggers audit risk and potential penalties exceeding initial investment gains.

Capital Gains and Reporting Burden

Each crypto transaction generates tax events. Swapping Bitcoin for Ethereum triggers capital gains tax in most jurisdictions. DeFi transactions (swaps, lending yields) multiply reporting requirements exponentially.

Institutions using DeFi protocols manage thousands of monthly transactions. Tax reporting software must track every transaction, calculate gains/losses, and generate jurisdiction-specific reports. Implementation costs run $50,000-$200,000 annually for mid-size institutional portfolios.

Tax complexity and regulatory uncertainty represent the largest operational barriers to institutional crypto adoption, not market volatility.

Many institutions postpone DeFi participation solely because tax treatment remains unclear. Waiting for clarity makes sense given compliance costs and audit exposure.

Pro tip: Engage tax counsel and compliance experts before deploying capital, as tax reporting requirements often exceed trading infrastructure costs and can retroactively impact historical returns if initial classification proved incorrect.

Integration with Traditional Finance Systems

Crypto and traditional finance are converging faster than most institutions realize. Banks now operate custody services for digital assets. Payment networks process stablecoin transactions. Clearing systems integrate blockchain settlement. This convergence reshapes how institutions think about infrastructure and operations.

The integration isn’t about replacing traditional systems. It’s about creating bridges where crypto’s speed meets banking’s stability. These hybrid systems will define institutional finance for the next decade.

Banking Infrastructure Adaptation

Major banks redesigned their technology stacks to accommodate crypto. They added digital asset custody, trading operations, and settlement interfaces. This required significant capital investment but unlocked new revenue streams.

Three infrastructure layers now exist side-by-side:

- Legacy systems: Existing clearing, settlement, and payment infrastructure remaining largely unchanged

- Crypto-native systems: Blockchain networks operating independently with their own consensus mechanisms

- Hybrid bridges: New infrastructure connecting traditional and decentralized systems

Your institution likely already operates within this hybrid environment even if integration wasn’t intentional. Stablecoin usage moves capital through blockchain rails while maintaining traditional banking relationships.

Interoperability and Settlement

Integration of cryptocurrencies with traditional finance reveals complex technical and regulatory challenges. Settlement timelines differ dramatically. Bitcoin transactions settle in 10 minutes on-chain. SWIFT transfers take 1-3 business days. Banks must now manage both speed profiles simultaneously.

Interoperability standards remain incomplete. Bitcoin doesn’t natively connect to Ethereum’s ecosystem. Neither connects cleanly to traditional banking rails. Bridge solutions (wrapped tokens, sidechain validators, liquidity pools) create conversion mechanisms but add custody and counterparty risk.

Your institution needs technical expertise to navigate these conversion layers. Mistakes in bridge selection cost millions in slippage or security breaches.

Institutional Products and Services

Banks now offer hybrid financial products combining crypto and traditional instruments. Cryptocurrency derivatives contracts use blockchain settlement. Tokenized bonds issue on Ethereum while maintaining legal compliance under traditional securities law.

These products serve two audiences:

- Crypto-native firms seeking traditional banking integration

- Traditional investors seeking crypto exposure without using public exchanges

Goldman Sachs, JPMorgan, and BNY Mellon all launched crypto service divisions. These units don’t cannibalize legacy revenue. They attract assets that previously went to pure-play crypto firms.

Central Bank Digital Currencies as Integration Catalyst

Central bank digital currencies represent the ultimate bridge. When CBDCs launch, they validate blockchain technology while maintaining monetary authority control. This regulatory blessing accelerates institutional adoption of crypto infrastructure broadly.

CBDCs create a common settlement layer. Commercial banks operate on top. Crypto protocols operate alongside. The interoperability problems partially resolve because CBDCs establish a trusted reference layer.

Central bank digital currencies will accelerate traditional finance integration with crypto faster than any market force.

Your institution should monitor CBDC rollouts in your jurisdiction. Launch timelines determine when legacy system upgrades become mandatory, not optional.

Risk Management in Hybrid Systems

Hybrid systems create new operational risks. Custody solutions span traditional banks and crypto-native firms. Settlement happens across multiple blockchains. Liquidity moves through novel bridge mechanisms.

Your compliance team must understand:

- Counterparty exposure across custody providers

- Liquidity flow through different settlement networks

- Regulatory jurisdiction for hybrid products

- Tax treatment when settlement happens on-chain

These risks aren’t theoretical. Institutions lost millions during bridge failures and custody breaches. Robust risk frameworks address hybrid-specific vulnerabilities, not just traditional or crypto-specific risks separately.

Pro tip: Build integration strategy on stablecoins and CBDCs first rather than pursuing full DeFi connectivity, as these assets have established banking relationships and regulatory clarity that reduce operational risk during system integration.

Navigate the Crypto Revolution Impacting Institutional Finance Today

The article uncovers the critical challenge institutions face integrating cryptocurrencies like Bitcoin, Ethereum, and stablecoins into established financial systems amid evolving regulatory demands and operational risks. If you are seeking to understand how decentralized finance, custody standards, and central bank digital currencies reshape global finance you are not alone. Many institutions struggle with volatility management, compliance frameworks, and building hybrid crypto-traditional infrastructure while maintaining competitive positioning.

Stay ahead of market shifts by getting timely insights about the macroeconomic impact and strategic considerations of crypto adoption. Visit Crypto Daily for the latest news on blockchain technologies, regulatory updates, and how key crypto asset types enable new financial models. Learn how major banks and regulators worldwide are responding to this transformation by exploring our comprehensive coverage.

Don’t let unclear regulations or operational uncertainty hold your institution back. Gain clarity on custody protocols, tax implications, and crypto market behavior now. Empower your team with expert analysis tailored for financial leaders ready to embrace digital asset integration. Visit Crypto Daily and start navigating your institution’s crypto strategy today.

Frequently Asked Questions

What are the main economic benefits of integrating cryptocurrencies into institutional finance?

Integrating cryptocurrencies can enhance cross-border efficiency, promote financial inclusion, increase market transparency, and provide new investment opportunities that are not directly correlated with traditional equity or bond markets.

How do stablecoins facilitate the transition between crypto and traditional finance?

Stablecoins combine the efficiency of cryptocurrencies with the stability of fiat currencies, allowing institutions to move capital quickly while mitigating the risks associated with price volatility.

Why is regulatory clarity important for institutional adoption of cryptocurrencies?

Regulatory clarity ensures that institutions can operate within defined legal frameworks, reduces legal uncertainties, and allows risk committees to justify crypto allocations to boards and regulators, ultimately accelerating adoption.

What role do central bank digital currencies (CBDCs) play in the integration of crypto into traditional finance?

CBDCs validate blockchain technology’s utility while allowing central banks to maintain control over monetary policy. They create a common settlement layer that can enhance the integration and efficiency of both traditional and decentralized financial systems.

Recommended

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.